The first Additive Manufacturing Europe show, which took place in Amsterdam from June 28th to the 30th and was sponsored by SmarTech Publishing — was tasked with the daunting challenge of helping the low-cost desktop 3D printing industry that it so well represented during the 3D Printshow years into a real and professional industry for accessible proto-typing and small series production. Led by Ultimaker and Zortrax the show and the industry now seem ready to enter into this new phase.

Ultimaker Takes the Lead

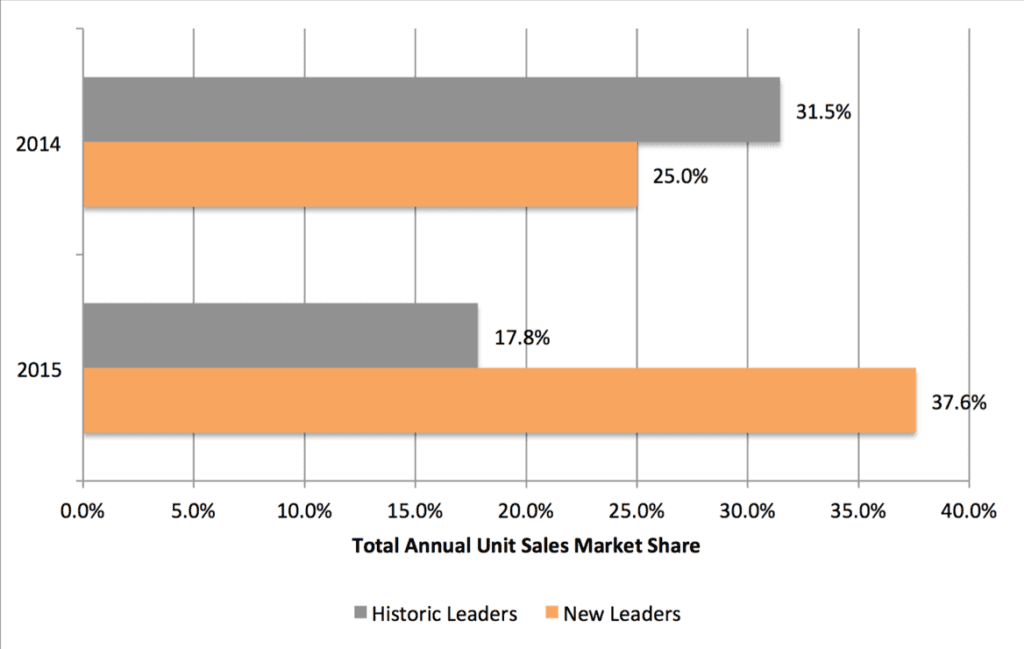

As anticipated by SmarTech Publishing in the recent Opportunities in Low-Cost 3D Printers: Technologies, Materials and Markets – 2016 report, Ultimaker has taken a leading role in the industry, successfully leveraging on the difficulties encountered by previous market leader MakerBot (not present with a booth at the show). Ultimaker CEO Jos Burger explicitly confirmed this to SmarTech Publishing stating that “we believe we are now market leader in the $2,000 to $5,000 segment”. Burger also added that, although Ultimaker believe they are currently number one, they have no particular in-terest in being alone, welcoming valid competition in order to help build the industry together.

Ultimaker’s large stand showed that the Dutch company is now ready to lead the desktop 3D printing market with solid international structure.

Joining Ultimaker two years ago, Mr. Burger helped the company shift from being a successful startup to a small multinational enterprise, building up to 210 employees globally and a strong presence in both Europe and North America (with a close eye on the APEC market). This is the way other desktop 3D printer manufacturers must follow and, although it is certainly leading, the AM Europe show demonstrated that Ultimaker is also not alone. Poland based Zortrax also was present with a large booth representing the success of its retail efforts over the past two years.

Prosumer Segment Heading Toward Industrialization

SmarTech Publishing is seeing other smaller companies such as Italy based Sharebot and WASP or Latvia based Mass Portal showed that they are investing in technological advancements that can help move the market in new directions. WASP presented a 3 meter tall multi-tool capable machine that can print directly from granules for cost optimization; Sharebot was present with a new version of its prosumer grade $9,000 DLP Voyager 3D printer integrating continuous DLP (C-DLP) for ultra-fast 3D printing. Mass Portal presented a new set of internally developed nozzles which enable its Delta architecture filament extrusion 3D printer to achieve resolutions comparable to high-end SLA.

Zortrax welcomed the prosumer challenge by releasing its new $5,000 M300 system.

In fact the first edition of the show also confirmed another one of SmarTech’s assessments for desktop 3D printing and specifically that the most valuable segment for future growth in this area is the prosumer segment. This is the range from above $5,000 to below $10,000. Zortrax, more aggressively than most other companies, is now finally targeting this area of development by choosing the AM Show Europe show as the venue for the announcement of its new M300 3D printer. This is a new system, very similar to the highly successful M200 but significantly larger, enabling a much wider range of applications.

Finding that Magic Price Point

Zortrax thus departed from the yet unreleased Inventure project for a smaller, consumer-focused desktop 3D printer. The Polish company listened to the market’s demands for a more prosumer-focused system and addressed them with a 3D printer that will be priced at around $5,000 (a significant departure from the current sub-$2000 price tag of the M200). The inverse trend (also described by SmarTech Publishing’s report) is also taking place, with more expensive technologies beginning to become more accessible in lower priced systems.

With its new Voyager WARP continuous DLP system, Sharebot leads the charge of the smaller companies bringing high-end 3D printing technologies into a low-cost, prosumer accessible range.

Sharebot is a clear example with the above mentioned Voyager WARP introducing low-cost continuous DLP and doing what its SnowWhite system is doing for low cost SLS. Other noticeable examples were 3Dee’s $20,000 full color binder jetting system from 3DPandora and South Korea based Rokit’s$20,000 dual extrusion bioprinter.

While we saw other interesting companies present with newly engineered system and materials, the Additive Manufacturing Show transition toward a more industry-centered approach is still only at the beginning, which means not many companies – other than EnvisionTec and Prodways – were present from the market’s high-end segment of 3D printer manufacturing. However it did set a solid foundation on which to build for the upcoming Additive Manufacturing Americas show in Pasadena next December and a great reason to return to Amsterdam in 2017.